At the beginning of the 19 th century British government revenues were gathered by four departments.

- Customs were concerned with duties on imported goods.

- The Excise Office dealt with duties on particular goods produced domestically. (The problems for the maltsters of Boxford referred to in Sisters and Brother came from a visit from representatives of the Excise.)

- The Board of Taxes gathered Land Tax and Assessed Taxes.

- The Board of Stamps oversaw the gathering of duties on licences and documents and other items carrying a Stamp Duty.

The history of tax administration in Britain is one of the amalgamation and reconfiguration of these different bodies. Stamps and Taxes were combined under the Board of Stamps and Taxes in 1834/5, while in 1849 the Board of Excise merged with the Board of Stamps and Taxes to create the Inland Revenue. Excise separated from Taxes to combine with Customs in 1909, and it was not until 2004 that Customs and Excise and the Inland Revenue combined to become the current HMRC – His Majesty’s Revenue and Customs.

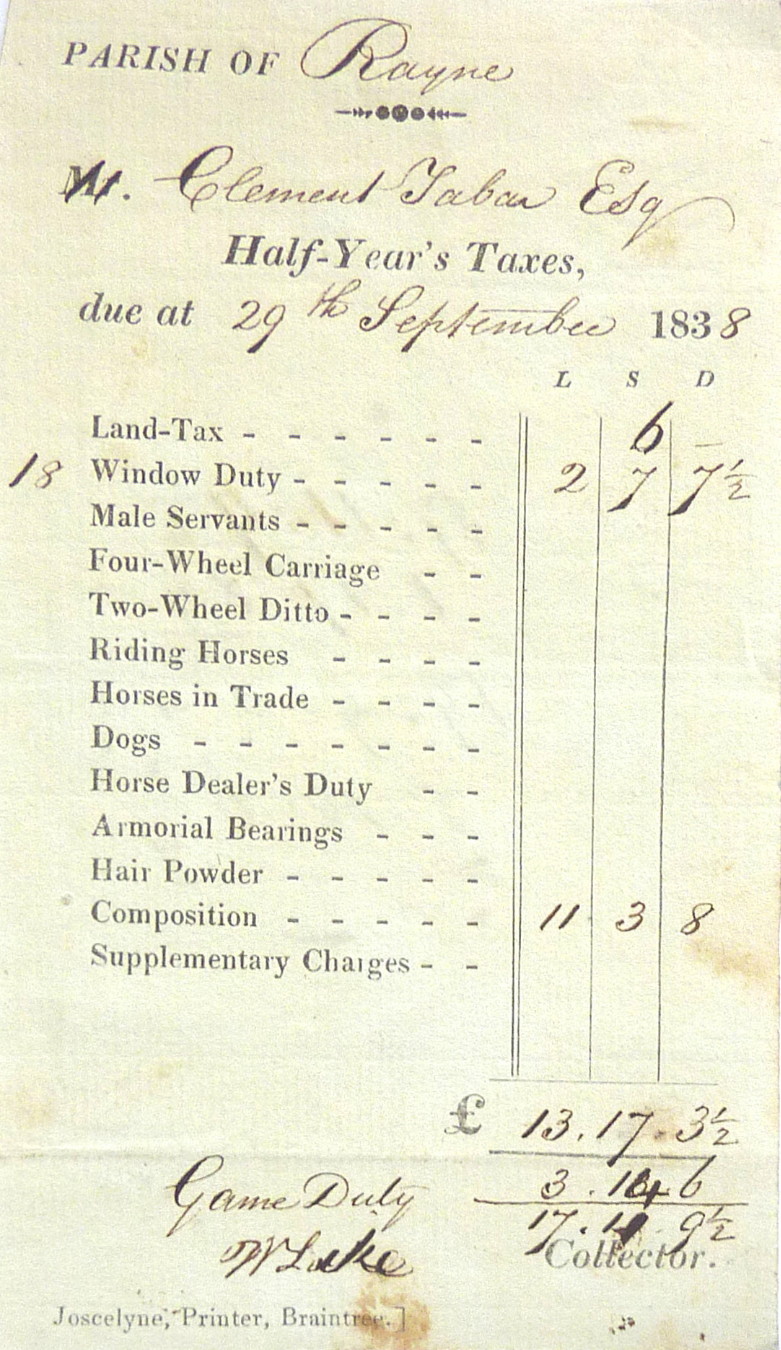

The 1838 bill shown here is for Assessed Taxes, falling under the Board of Stamps and Taxes. Payments would have been gathered by one of the Collectors appointed by a parish Assessor, himself appointed by a District (or Division) Commissioner. Taxes were still being paid half-yearly at this time. Notably, the due date for payment is shown as 29 th September. This is is Michaelmas Day, one of the traditional Quarter Days (the others being Lady Day, Midsummer Day, and Christmas Day) which had long been associated with payments of rent and other debts. This is despite the fact that the official beginning of the tax year had been moved 11 days from the traditional March 25 th date of Lady Day to April 5 th in 1752/3 -adjusted a further day in 1800 – in response to Britain’s move from the Julian to the Gregorian calendar.

To the modern reader, perhaps the most obvious thing about the bill is how little it resembles the personal tax assessments received in the 21 st century. For one thing, it includes no tax on income.

In fact, an Income Tax had been introduced in 1799, as a temporary measure to help fund the war against Napoleonic France. But, following the defeat of the Napoleonic forces, the unpopular tax was repealed in 1816 (there had already been a brief lifting of the tax between 1802 and 1803). Later pressures on government finances would see it return, in 1842, since when it has remained with us. So, the 1838 bill falls within a gap in the history of Income Tax in the United Kingdom. This makes it feel closer to assessments made in the 18 th century tradition of taxation, the liability being composed of many different taxable elements.

Land Tax, which appears first in the assessment, is the oldest form of direct taxation in Britain. While there were earlier levies related land ownership, a tax on land, property, and possession of public offices was established by Parliamentary Act in 1692. The tax had to be voted for annually by Parliament until 1798, when it was made permanent (though it could be redeemed by paying a lump sum equivalent to 15 years charge). With amendments Land Tax continued until1963.

Window duty, a tax levied on the basis of the number of windows in an owner’s property, had also first appeared in the 17 th century, in 1696. Initially the tax was imposed, as an addition to a basic house tax, on properties with more than ten windows, reduced to seven in 1776. Though often regarded in recent times as one of the stranger tax choices, there were those who argued for it as less-intrusive alternative to an income tax. The better-off, it could be claimed, were likely to own properties with a higher number of readily-visible windows. Assessment based on these did not require access to personal financial information. But it became apparent that window duty had other consequences, which would lead to it being described as a tax on light and air, with a serious impact on health. These effects became increasingly clear with growing urban working populations, the owners of their dwellings having financial incentive to minimise the available light and ventilation. Yet established taxes often have an inertia which makes them difficult to shift. It was not until 1851, after substantial campaigning that window tax was removed.

Most of the other components of the 1838 assessment involve taxation of particular consumption choices. A tax on the employment of male servants had been introduced in 1777, by a government seeking funding for the conflict in the American colonies, and would continue for more than a century. Duties on ownership of carriages and horses also had origins in the 18 th century, Carriage Tax appearing in 1747, and a tax on saddle and carriage horses imposed in 1784. The tax on horse dealing operated at higher rate in the immediate area of London, but was applied throughout “England , Wales, or Berwick upon Tweed” (Berwick presumably being specified because of its historically marginal position between England and Scotland).

Pressures for a tax on dogs, in part, had come from those concerned about dog control and the risks arising from a large population of dogs (including rabies). But, again, it seems to have been the need to fund the war with Napoleonic France that sealed its introduction in 1796. The taxpayers would be the keepers of sporting dogs, window tax payers with a non-sporting dog, and keepers of packs of hounds. With some success as a wartime revenue spinner, a special tax on greyhounds was added in 1812. Dog duty would continue, changing from an assessed tax to an excise license later in the century. A dog licence requirement existed in England until 1987.

The possession and use of personal and family heraldry was also subject to tax. Anyone displaying armorial bearings, such as a coat of arms painted on a carriage, had been subject to a duty from 1798, this becoming an Assessed Tax in 1801, with its scope clarified and extended. For instance, employers were explicitly made liable for tax on any armorial bearings shown on the liveries of their servants. The tax was altered to an Excise Licence in 1869, but not removed entirely until 1944.

The duty on hair powder was another charge introduced during the wars with France, in 1795. By 1838 the use of powdered wigs and powder on hair was already substantially a fashion of the past. The tax itself had helped to encourage its decline. By 1855 less than 1000 people were paying it. But this is another tax which lived on for decades, despite a declining yield. It was not removed from the statute book until 1869.

Game Duty, the levy on anyone wishing to hunt game, has had to be written in by hand at the end of the assessment, though it had become an Assessed Tax thirty years earlier (replacing Stamp Duty on game certificates). Parliamentary Acts of 1784 and 1785 required anyone with a “dog, gun, net or other engine for the taking or destruction of game” to register each year with the clerk of the peace and pay a fee for a game certificate. In legislation of 1808 the collection of fees and issuing of certificates shifted to the Collectors of Assessed taxes.

For the person who received the bill shown here we have no details of liability for many of its components, because he has opted to pay a composite charge -‘Composition’. At this time taxpayers could choose to ‘compound for’ assessed taxes. For a percentage addition to an initial tax assessment they could hold their liability unchanged for several years, three in the first instance, despite changes in their circumstances (an upgraded carriage, more windows, more servants, etc.) that would otherwise have increased it. This compounding of taxes is one source of difficulty for anyone wanting to analyse the specifics of tax payments in this period.

The total payment here is substantial. We are looking at an assessment on a well-off householder, whose total tax liability for the year may well exceed the annual income of poorer families.